[Author’s note: Thank you for your support thus far! If you haven’t yet, please subscribe. If you already have (or even not), please share with your networks. It’s free and helps compound the growth of the community, which is all this newsletter needs to continue creating content.

I will hopefully be ramping up the speed of pieces before a summer hiatus — upcoming topics include:

— Primer on commodities (metals & minerals)

— China’s role in the global system

— Understanding renewable energy & decarbonization

— Ecological crisis, not climate crisis

— Global development & the return of industrial policy

Some other exciting developments coming up soon as well!]

“The monetary system is designed to be hidden.” - Jeff Snider

“The costs of the dollar's status as the international reserve currency now outweigh the benefits, and the United States should take the lead in moving to multi-currency reserves.” - Michael Pettis

Introduction

In recent pieces I have talked about how the recent hype about de-dollarization is wrong. In this piece, I go further and explain how the mainstream understanding of the US$ system itself is flawed because it leaves out critical features and markets.

If you think being the global reserve currency (GRC) is a huge benefit to the US people or that the US$ system is some centrally controlled policy run by the US government (and central banks), this piece should offer some interesting provocations.

I cover 3 parts here, which I hope will provide a simple yet comprehensive way to think about this topic:

What is a global reserve currency?

How the US$ ended up here (including the most important financial market you’ve probably never heard of).

Why de-dollarization is hard, and how we are painfully stuck in a dying system.

To understand the US$, global trade, and the second order impacts such as geopolitics, US-China decoupling, etc., it is important to know what money is and how it works – the standard conception is wrong and leads to errors cascading through other analytical domains.

Anyways, here’s the 1-min summary of this piece:

→ The US$ system makes the global system run and hence it must be integrated into political/policy analyses more often.

→ The weaponization of the US$ against Russia, Afghanistan, etc. recently has exacerbated a long-term trend of using the US$ for geostrategic gains (swap lines are a good example).

→ Many countries across the Global North & South are looking to diminish their reliance on the US$ for a myriad of reasons (sovereignty, debt crises, etc.)

→ However, no country wants to (or even can) take up the mantle because of the domestic hardships that the GRC country must experience.

→ The US$ system is run through a decentralized, unregulated and private global banking system, not through central bank policies per se. Banks, shadow banks, and other financial entities run the show!

The Making Of A Global Reserve Currency

Money is simply a tool that mediates financial transactions and commerce. That’s the primary objective. In order to do this holistically, the GRC is more than just the currency we conduct global trade in; instead, it is a multi-faceted, comprehensive system and must be understood as such.

There are 5 key features to think about:

Pricing: Pricing goods (say oil) in multiple currencies is significantly more complex than simply pricing it in one currency across time and space. With the lower transaction costs and greater coordination that comes with using the same unit of account, more and more economic agents begin adopting it, leading to network efforts. This bottom-up phenomenon is coupled with, and maybe even driven by, the top-down imposition of a specific currency.

So one function is a standardized form of pricing goods & services so as to make trade more efficient.

Supply/availability: Each currency is the creation of a specific sovereign entity. When it comes to the GRC, one country issues it and the rest of the world needs some way to access it. This means that the issuer of the global reserve currency must be willing to supply the global economy with its currency.

Some ways to do that include running a perpetual trade deficit (you buy more from the rest of the world than you sell, allowing foreign countries to net earn your currency) or by heavily investing abroad. The US does the former, while in the previous system under the British sterling, the latter approach was used.

This includes emergency lending when needed to protect the system from breaking. US$ swap lines, IMF lending, all sorts of borrowing facilities created by the US Fed, etc. are hence forced onto the US.

So that’s the second thing: the issuer must supply the world with its currency. This is why the US must run trade deficits and act as a global lender of last resort!

Savings & investments: Say Brazil has a trade surplus against the US (meaning it earns US$). Once it has those US$, it needs to be able to invest them in order to build reserves for the future. This means that it needs access to US$-denominated assets: bonds, stocks, real estate, etc. For Brazil to have that, the US must be willing to have open financial markets and absorb these Brazilian financial inflows, allow foreign ownership of US assets, etc.

The Asian Financial Crisis of the 1990s occurred because high-performing developing countries (Thailand, etc.) were running trade deficits and hence relied on foreign US$ investment to cover the gap. When that investment suddenly went away, their currencies crashed, and chaos ensued.

This experience taught other developing countries that the only way to be protected is to run trade surpluses against the US and stockpile the US$ (in the form of US assets). China’s massive US$ reserve stockpile, along with that of Taiwan, Singapore, Korea, etc., is explained by this dynamic. The US has to then absorb all these financial flows because these surplus nations want to park their cash somewhere, ideally with a positive return on investment.

Both sides – the US and the trade surplus developing countries – are forced to act this way by the system.

Institutional support: The system requires that the GRC issuer is trustworthy, stable, and transparent, at least to an extent.

There needs to be a robust and trusted legal system to settle disputes (which is why a lot of debt issues for example get settled in NYC), the GRC issuer needs to have domestic stability so that all the features explained above remain consistently active, and there needs to be sufficient geopolitical trust and cooperation. Military might, policing of trade routes, and the ability to enforce compliance are also inextricable from this mix.

This is why the GRC issuer is typically always the global hegemon and why the weaponization of the US$ causes geostrategic tremors.

Domestic economic management: The economy is a set of interlocking balance sheets such that it is impossible to influence one end without doing so with the other. This means that all the aforementioned features (trade deficits, open financial markets, etc.) have domestic counterparts which must be applied and managed.

For example, the US$ system requires the US to have open financial markets to absorb the US$ savings of the rest of the world. This means that this liquidity is ending up on domestic balance sheets as liabilities (debt), which is why US households are heavily indebted, while Chinese households have excessively high savings (both are a problem).[More on this later]

Not all features are equally important though. For example, given the evolution of digital banking and the liquidity in financial markets, it almost doesn’t matter what currency you conduct trade in since anything currency can be instantly exchanged for the US$. What matters is what countries do with whatever currency they receive.

Ultimately, no currency regime is perfect or sustainable. Like everything else, they run with the cycle of history and are subject to a myriad of political, geopolitical, and economic forces.

Here’s an illustration of the history of global reserve currencies.

[I would take this chart with a grain of salt because the specific setup of GRCs has evolved over the centuries, as the level of globalization has changed, but the general principles hold]

“The dollar is our currency, but it's your problem.” – John Connally (Nixon’s Treasury Secretary), 1971.

Let me start by recapping the conventional story about the US$ (aka the petrodollar) that most people know by now:

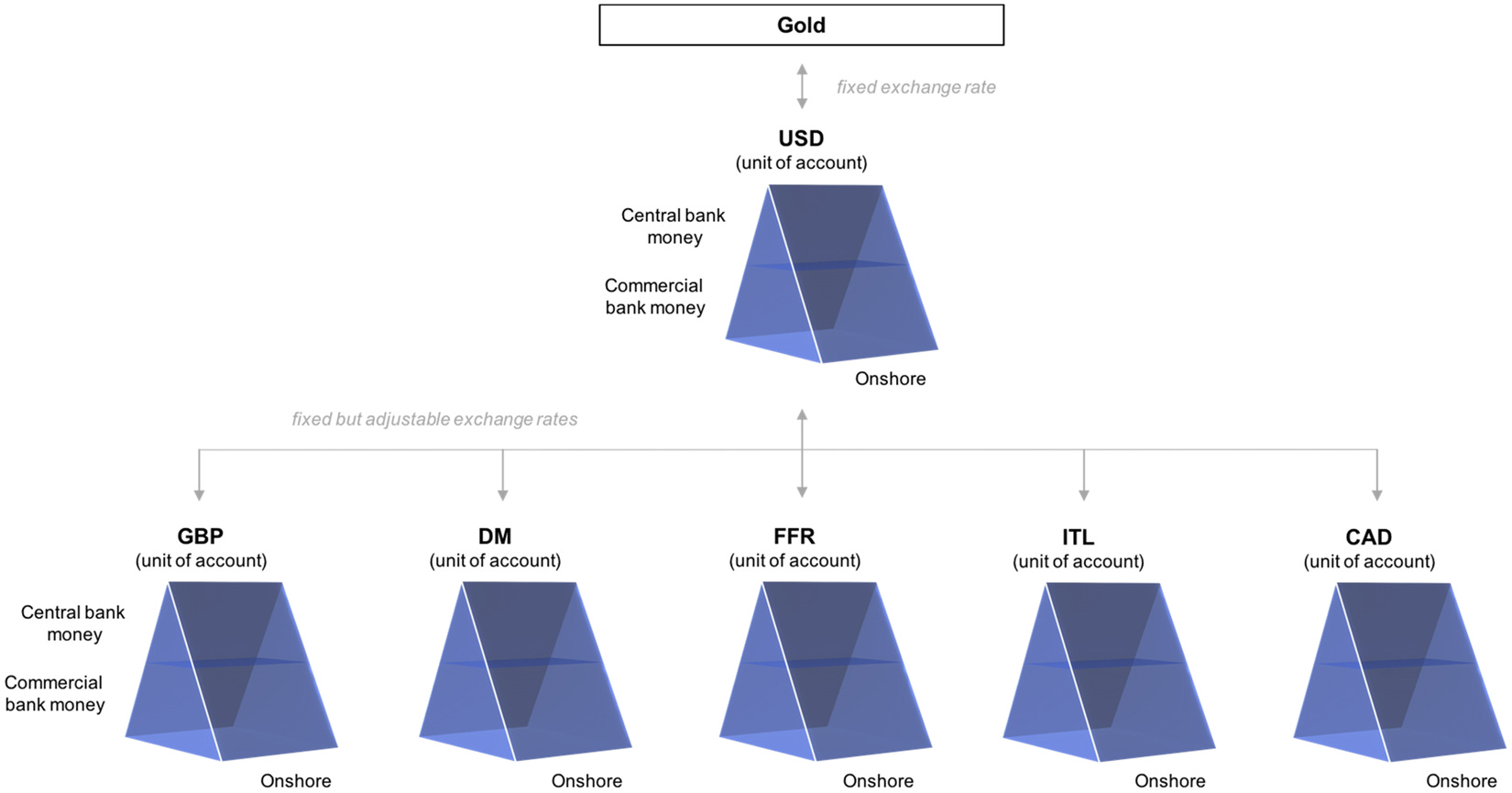

Post World War II, the Allied Powers held a session at Bretton Woods to establish the new global system. The discussion was primarily between England (the sunsetting empire) and the US (the established hegemon by then), resulting in a system where all currencies had a fixed exchange rate against the US$, while the US$ was “backed by gold”. The US was also largely financing the recovery of Europe, which is why this system seemed to make sense.

[The history of this is interesting because John Maynard Keynes (representing England) and Harry Dexter White (representing the US) had competing proposals about what to do with the global system and although White won – leading to the US$’s role – they both agreed that the free flow of capital needs to be limited. Hopefully by the end of this piece it will be clear why free, unregulated capital is a problem.

Note: This system was designed without any Global South representation, and yet somehow the IMF & WB, which came out of this, are supposed to work for global development.]

Then in 1971, as the US had to finance its invasion of Vietnam, the shift from a US trade surplus to a trade deficit, and with European countries (primarily France) applying pressure on the US regarding whether it had sufficient gold reserves to back its spending, President Nixon oversaw the end of the Bretton Woods 1.0 system. To replace this system, the US cut a deal with major oil exporters (primarily Saudi), to establish the petrodollar: Saudis would sell oil in US$ globally, and since all countries need oil, everyone would need US$.

The simple version of this is that when a Turkish construction company, for example, wants to buy steel from China, it borrows US$ from a Japanese financial institution to make the transaction happen. The Chinese steel manufacturer then uses those US$ and pays a Brazilian mining company for the iron ore. Since the Brazilian company has a bank account in a French bank, the US$ move from the Japanese to the French entity. At no point in these transactions was a US government agency, bank, or company involved, yet US$ were created (through borrowing) and used.

[Foreign offices of US banks & companies do participate in the system but those are not under US regulation.]

You may say well what’s controversial or insightful about this – if some non-US countries have surplus US$ lying around, they can lend it to whoever they want. But this is where understanding money and banking correctly is critical (and why newsletters #4 and #5 went deep into this).

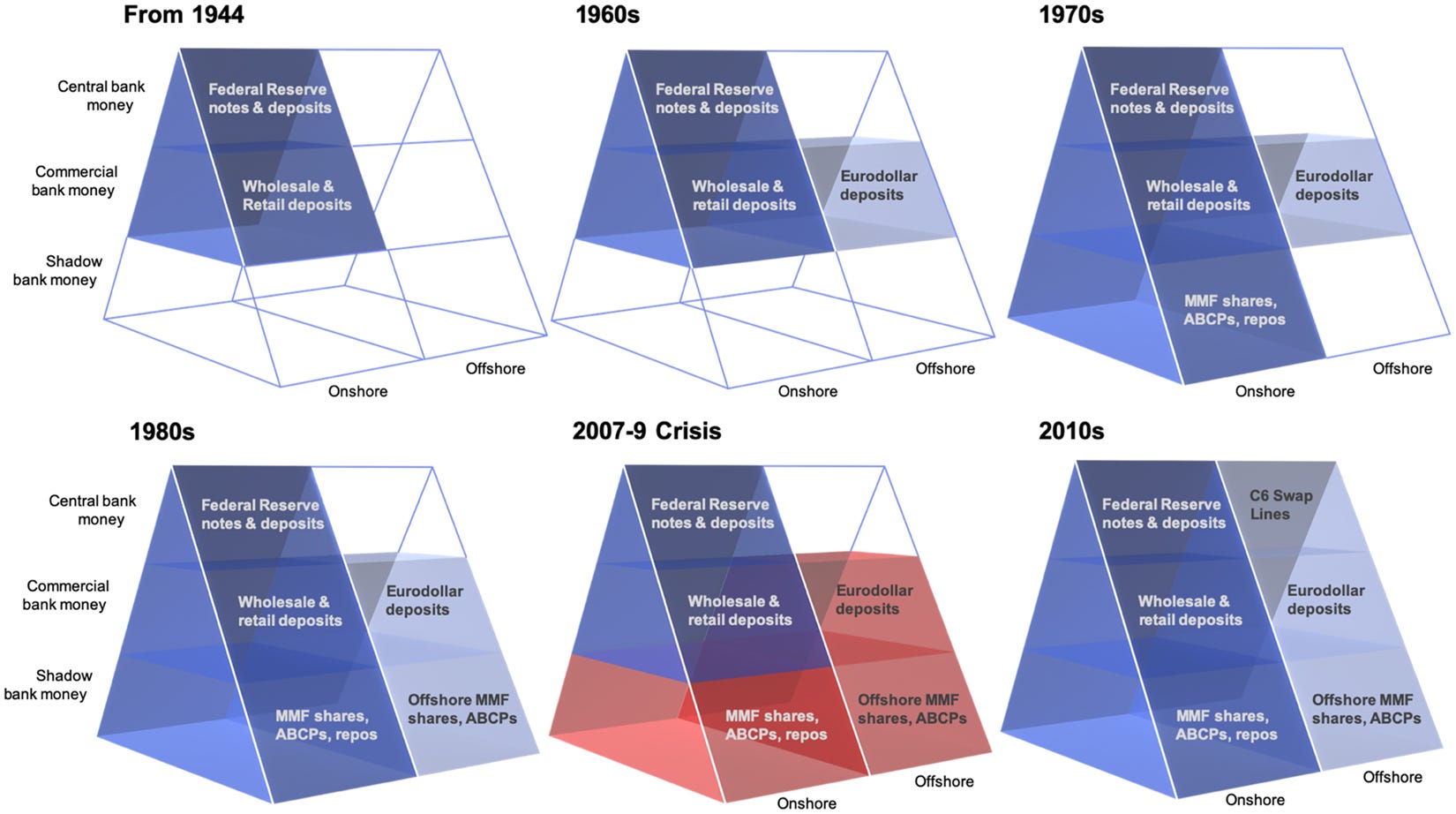

Eurodollars are not just stacks of dollars that a country earned and has stored; instead, they are US$ *created* by non-US banks.

Recap: money (today at least) is debt. Money gets created when a government or its chartered entities (banks) increase its liabilities. When the government spends, money is created. When banks lend, money is created. It is a liability on the issuer’s balance sheet and an asset on the receiver’s balance sheet.

The US$ is a liability of the US govt so of course it can create this currency. US banks can also do that because they are chartered entities under the regulation and payment system of the US government. But how can non-US banks, and here I use the word banks loosely because it’s more than just commercial banks, create US$ when they have no conventional access to the US Federal Reserve (the bank of banks)?

In the words of Milton Friedman, whose essay was one of the first real explanations of the Eurodollar system, this is: "the latest example of the mystifying quality of money creation to even the most sophisticated bankers, let alone other businessmen." For him, the Eurodollar, like all money today, is the “creation of the bookkeeper’s pen”.

Realistically how this worked is that as large amounts of money was flowing from the US to Europe to finance the reconstruction efforts, non-US entities started accumulating US$. They then used these US$ holdings to start lending out “eurodollars” (a promise to pay in US$). So a holding of say $100 billion could be used to create $1 trillion worth of loans. Again, this is how money creation works. If both the issuer and the receiver agree to value a paper claim (liability), and then other agents will accept those claims as payments, the system works.

And since everyone in the world needed US$ for trade, even before the petrodollar existed, the Eurodollar system became the primary source of US$ funding in the world. The US government facilitated this because it eased the pressure on it to manage the supply of US$ to the world.

The reason I try to explain this carefully is because this changes how we analyze the US$ system. The conventional story is quite state-centric, predicated on there being a masterplan skillfully executed by a group of bureaucrats and technocrats. The latter, in fact, centers the role of the market and sees the current system as a spontaneous evolutionary process shaped by shifting dynamics and emerging crises, leading to a starkly different analysis.

Here are 5 ways this story changes about how we understand the global system and the US$:

The US$ was “chosen” by a broad swath of market agents (the “market”) because it was deemed to be the best fit for what was needed in order to make global trade most efficient.

The Eurodollar system is the main financial engine for the global economy (it was instrumental in financing China’s development for example). One market connecting together sovereign nations, banks, conglomerates, traders, etc.

It is a decentralized, market chosen system that creates unregulated money (laissez faire on display).

Nixon in 1971, by ending the Bretton Woods 1.0 system, was actually trying to relieve the US of the burden of being the GRC. The Eurodollar system stepped up to fill the void and eventually forced the US into a position where it had to support this offshore market. The unprecedented Reagan era financial deregulation, removal of capital controls in 1983, and continued financial innovation by the Fed to backstop the global system can be seen as a part of this.

The extent to which this system runs on trust is very high, given that this funding is all just non-government backed IOUs/liabilities built on top of each other. Remember the hierarchy of money I have talked about in previous pieces. Eurodollars, as shadow money, are at the riskiest end of the pyramid. Fictitious capital, perhaps.

This is why in the 2008 financial crisis, the majority of US Fed emergency lending went to European banks. This is why swap lines are so important. This is why the US Fed keeps innovating ways to provide US$ liquidity to players well outside its domain. This is why Japan (which is arguably the main node of the Eurodollar system as it lends to China and other Asian countries) is so important.

This is also why the US-China decoupling is so hard, why de-dollarization is not up to world leaders to announce their intents to change, why all nations (incl. the US) are stuck in a broken global economic system, and why the situation is so precarious right now as geopolitical risk and financial instability could cause serious havoc.

Lastly, this is why critics of the current monetary system who talk about “central planning”, government debasement of currency, money supply increase, Bitcoin, etc. are missing the point.The Eurodollar is an unregulated, opaque system left to the whims and innovations of a broad group of global market participants. We don’t even know how much money exists in this system, let alone who owes how much to whom. And yet people, including Central Bank chairs and economists, talk about measuring the money supply and interest rate hikes as the primary controls over the monetary system.

It’s like trying to manage the water in a swimming pool by focusing on 1-2 pumps in a corner, with no visibility on other pumps, drains, the shape of the pool, etc.

We already live in a world with a decentralized, market driven system run by finance that simultaneously tussles with and relies upon a group of bureaucrats and technocrats. It is a key example of how “market driven” doesn’t mean democratic or equitable or beneficial for the mass majority.

Reality is a lot more complicated.

The US$ hegemony, the IMF/WB, etc. have at least been routinely criticized for their role in economic crises globally; but as Jeff Snider remarked in the quote at the start, the success of the Eurodollar system is its ability to stay hidden and remain beyond critique, despite being the driving force of the system.

Now we can combine the explanations in part 1 and 2 to better understand what the US$ system is, and hence make more informed analysis about global events and the future. Since finance & money is the water in which we all swim, there are multiple layers in terms of implications but let me focus on 3 for now:

US economic development

The phrase “exorbitant privilege” gets thrown around a lot regarding the US$’s special status, as if the US as a whole benefits from being the GRC. That is far from the truth.

Becoming the linchpin of the global financial system has benefitted Wall Street, Silicon Valley and related elite groups globally at the expense of the real economy and the working class – manufacturing, industry, etc, – turning the US into a financialized, speculative country with burgeoning inequality, crumbling infrastructure, etc. The government has the unenviable task of managing domestic development while backstopping a global, complex financial system that it didn’t create and can’t oversee.

For example, if the US wants to rebuild its manufacturing, it needs to import less, maybe have a weaker exchange rate (to make local goods more competitive), definitely limit the inflow of global financial savings (the US has sufficient investment), and have monetary policy designed for domestic needs. All these, however, would pull the rug from under the global financial system, which would ultimately harm the US because of how interconnected the global economy is.

Dollar shortage, not de-dollarization

Since the global economy is just a set of interlinked balance sheets (the Eurodollar system represents that in its purest form), then it’s much easier to think about de-dollarization. There are trillions of dollars of liabilities and debt denominated in US$ which can’t simply be wished or ordered away. Can you imagine an orderly way for those liabilities to be unwound or settled in another currency? Given the coordination required, I for sure cannot.

In fact, the recent hype about de-dollarization actually reflects the brewing pain underneath the surface as countries begin to face a US$ shortage, which of course leads to terrible outcomes like financial crises and economic misery. A combination of higher US interest rates and a faltering Eurodollar system are sucking out US$ liquidity from the global system. De-dollarization narratives may then actually be a cry for help.

💡Lastly, can you think of any country willing to shoulder the burden of this global financial system? For example, an integral part of Chinese development are strong capital controls and a highly regulated banking system. Is China going to give that up to the whims of the global finance market? Highly unlikely.

Global development, Chinese lending, and sovereign wealth funds (SWFs)

There are 3 types of countries in the world: those with huge US$ reserves (China, Singapore, etc.); those with sufficient reserves (e.g. Brazil, India); those with chronic US$ shortage (e.g. Argentina, Pakistan). All are facing their own challenges in this system.

The ones with huge reserves have accumulated them by suppressing domestic development so that wages are low, imports are limited, and savings are high. This creates the trade surplus which allows US$ accumulation. This is an unsustainable system. On top of that, these countries now need to get creative about what to do with the US$.

The Belt & Road Initiative (BRI) represents China’s attempt to use its US$ reserves in a way that does not involve buying US assets but as it is finding out, similar to how the US found out in the early 20th century, investing in emerging markets is quite risky. The growth of SWFs, particularly in the Middle East, along with investments in trying to build futuristic cities in the middle of the desert, are also just attempts to break away from the earlier model of simply buying US assets.

The ones with sufficient reserves are stuck in a specific development model where they must ensure trade surpluses to protect themselves from a US$ shortage – basically the present – but that involves all sorts of domestic development trade-offs, continued reliance on the US$ system, etc.

The one’s without US$ are, of course, stuck in a perpetual doom loop (which I explained using Pakistan’s example in newsletter #5). Being able to tap a liquid Eurodollar system, for example, has been a vital avenue for trudging along but now with that even faltering, large swathes of the global population are at serious risk of negative food, energy, etc. shocks.

Slightly tangential point on the Global South: even under this postcolonial, US$ system, there exist 14 countries in Sub-Saharan Africa (formerly colonized by the French Empire) that are still forced to use the CFA Franc, which is a colonial currency controlled by the French government. A literal colonial policy that continues to be enforced.

Here’s a podcast where Ndongo Samba Sylla (who recently wrote a book on this topic) explains.

If you have been convinced by something thus far, please share — it’s free!

This is the trillion-dollar question and frankly, no one has an answer. All we know is that the post Bretton Woods system is broken, and arguably has been since the 2008 Financial Crisis which is why global growth has been so sluggish. The current system doesn’t work for the people of any country, it only enriches the financial elite and rentier class.Trade wars are class wars!

Here’s what we do know: the current push towards industrial policy, reshoring manufacturing in the Global North (led by the US), efforts to decouple from China, etc. cannot be done under the current regime. Just for the US alone, its attempts to develop domestic supply chains and manufacturing capability is at odds with the GRC status.

On the other hand, countries have massive US$ debts in a system with rapidly drying up liquidity.

Most likely the situation will require coordination and compromise – a la Bretton Woods – but increasing geopolitical tensions are a minefield for that.

I leave you with this is excellent discussion between two godfathers of understanding the global financial system — Zoltan Pozsar & Perry Mehrling — on what could replace the status quo, as well as this great piece on the need for a “Bandung Woods”, rather than a new Bretton Woods, to create a system that actually serves a majority of the global population.

Thanks for reading Fictitious Capital! Subscribe for free to receive new posts and support my work.

And yes, I kinda agree with what Richard Werner says (and maybe what Minsky said) about democratizing finance by having more regional/community banks that are focused on underwriting and backed by a public guarantee system.

I first heard of Eurodollars in a book by "Adam Smith" (George J. W. Goodman) called "Paper Money" which came out in 1981. I was wondering if you had heard this story about its origins. I haven't seen it anywhere else. The relevant portion is below (all typos are my own):

The Eurodollar was invented by the Russians.

Like everyone else in the mid-1950s, the Russians used the dollar in their international transactions. It was the key currency; no one wanted rubles. If you earned dollars, you could take those dollars to the United States and get oil, aircraft, wheat, soybeans, automobiles; you could also get, if you wanted it, gold. You could leave the dollars in a New York bank and get interest. Like everyone else, the Russians had some dollars in New York.

After the Hungarian revolt in 1956, a Russian bureaucrat moved his country's dollar balances to the Moscow Narodny Bank in London, a bank with a British charter owned by the Soviet Union. He probably thought that if the cold war got worse, the Americans might freeze those dollars in New York, so he had better keep them in Europe, beyond the reach of politics. I once pursued this faceless bureaucrat who deserves a footnote in history. The pursuit looked promising when a Russian banker said, "Dregasovitch didn't invent the Eurodollar, the people under him did; he just took all the credit," but the trail grew cold after that. The Eurodollar's inventor has disappeared into the complex world of Russian banking...

Pressed for details, the Moscow Narodny Bank replies with very dry tracts on "the development of socialist banks." It no longer matters. On February 28, 1957, the Moscow Narodny Bank in London put out to loan, through a London merchant bank, the sum of $800,000. This minuscule amount was borrowed and repaid outside the U.S. banking system. The Soviets also owned a bank in Paris called the Banque Commercial pour l'Europe du Nord, whose Telex address was "Eurbank." The Paris Russian bank took some Narodny dollars and lent them; the dollars were known as Eurbank dollars, and finally Eurodollars.

At that point we can retire the Russians from the history of the Eurodollar; the capitalist bankers all loved the idea. The charm of Eurodollars, to bankers, was that they didn't belong anywhere and owed no allegiance to anyone; therefore, nobody regulated them. They were beyond the reach of the Federal Reserve, the Bank of England, the Bundesbank, and all the other government authorities. The Federal Reserve can require banks to put up a portion of their deposits as reserves; other agencies govern the character and size of loans. But not in Eurodollars; these dollars could be deposited, lent, and repaid, all while the Federal Reserve looked on from afar...

So the regulation of the banks varied from country to country. But the *currency*, once escaped, was gone: there was no way to whistle it home. If threatened with regulation, the Eurodollars would flutter up like a frightened flock of warblers and alight in some other country.

Beyond the wonderful country of Euroland was a still more wonderful country called Offshore. In Euroland the dollars were lent and deposited beyond the reach of the monetary authorities. For the dollars that belonged nowhere, there were now countries with hundreds of banks whose banking systems did not exist, like the Bahamas, the Netherlands Antilles, and the Cayman Islands. The borders of the two countries, Euroland and Offshore, were very fuzzy and overlapping, and in any case the two countries existed by their nonexistence in the filing cabinets of big law firms in New York and London. The Netherlands Antilles would get to sell a charter, and some annual stamps, so it was happy; and the bank was happy because it was in the Big Rock Candy Mountain of banking, where bankers are free as the breeze. The banks might be small or they might have recognizable names...all chartered offshore and doing business in Euroland.

The currency for Euroland came from the balance-of-payments deficit, that is, from more dollars going out than coming in. If the extra dollars for Volkswagens had all come back to New York to be lent or invested, there would have been no Eurodollar. But some of those dollars, sent out, never came back; they arrived in Euroland with Caribbean tans.

This phenomenon began with the $800,000 loaned by the Moscow Narodny Bank in London, and now there are somewhere around three-quarters of a *trillion* dollars of this very fecund currency, and there are also Euromarks and Euroyen and Eurofrancs, all looking rested and tanned and showing no desire to go home.

The problem with those Eurodollars is that they *could* come home; they did not have to stay contained in their own wonderful world. What if there were too many of them?

How would you have framed it?

And yes, I kinda agree with what Richard Werner says (and maybe what Minsky said) about democratizing finance by having more regional/community banks that are focused on underwriting and backed by a public guarantee system.

I first heard of Eurodollars in a book by "Adam Smith" (George J. W. Goodman) called "Paper Money" which came out in 1981. I was wondering if you had heard this story about its origins. I haven't seen it anywhere else. The relevant portion is below (all typos are my own):

The Eurodollar was invented by the Russians.

Like everyone else in the mid-1950s, the Russians used the dollar in their international transactions. It was the key currency; no one wanted rubles. If you earned dollars, you could take those dollars to the United States and get oil, aircraft, wheat, soybeans, automobiles; you could also get, if you wanted it, gold. You could leave the dollars in a New York bank and get interest. Like everyone else, the Russians had some dollars in New York.

After the Hungarian revolt in 1956, a Russian bureaucrat moved his country's dollar balances to the Moscow Narodny Bank in London, a bank with a British charter owned by the Soviet Union. He probably thought that if the cold war got worse, the Americans might freeze those dollars in New York, so he had better keep them in Europe, beyond the reach of politics. I once pursued this faceless bureaucrat who deserves a footnote in history. The pursuit looked promising when a Russian banker said, "Dregasovitch didn't invent the Eurodollar, the people under him did; he just took all the credit," but the trail grew cold after that. The Eurodollar's inventor has disappeared into the complex world of Russian banking...

Pressed for details, the Moscow Narodny Bank replies with very dry tracts on "the development of socialist banks." It no longer matters. On February 28, 1957, the Moscow Narodny Bank in London put out to loan, through a London merchant bank, the sum of $800,000. This minuscule amount was borrowed and repaid outside the U.S. banking system. The Soviets also owned a bank in Paris called the Banque Commercial pour l'Europe du Nord, whose Telex address was "Eurbank." The Paris Russian bank took some Narodny dollars and lent them; the dollars were known as Eurbank dollars, and finally Eurodollars.

At that point we can retire the Russians from the history of the Eurodollar; the capitalist bankers all loved the idea. The charm of Eurodollars, to bankers, was that they didn't belong anywhere and owed no allegiance to anyone; therefore, nobody regulated them. They were beyond the reach of the Federal Reserve, the Bank of England, the Bundesbank, and all the other government authorities. The Federal Reserve can require banks to put up a portion of their deposits as reserves; other agencies govern the character and size of loans. But not in Eurodollars; these dollars could be deposited, lent, and repaid, all while the Federal Reserve looked on from afar...

So the regulation of the banks varied from country to country. But the *currency*, once escaped, was gone: there was no way to whistle it home. If threatened with regulation, the Eurodollars would flutter up like a frightened flock of warblers and alight in some other country.

Beyond the wonderful country of Euroland was a still more wonderful country called Offshore. In Euroland the dollars were lent and deposited beyond the reach of the monetary authorities. For the dollars that belonged nowhere, there were now countries with hundreds of banks whose banking systems did not exist, like the Bahamas, the Netherlands Antilles, and the Cayman Islands. The borders of the two countries, Euroland and Offshore, were very fuzzy and overlapping, and in any case the two countries existed by their nonexistence in the filing cabinets of big law firms in New York and London. The Netherlands Antilles would get to sell a charter, and some annual stamps, so it was happy; and the bank was happy because it was in the Big Rock Candy Mountain of banking, where bankers are free as the breeze. The banks might be small or they might have recognizable names...all chartered offshore and doing business in Euroland.

The currency for Euroland came from the balance-of-payments deficit, that is, from more dollars going out than coming in. If the extra dollars for Volkswagens had all come back to New York to be lent or invested, there would have been no Eurodollar. But some of those dollars, sent out, never came back; they arrived in Euroland with Caribbean tans.

This phenomenon began with the $800,000 loaned by the Moscow Narodny Bank in London, and now there are somewhere around three-quarters of a *trillion* dollars of this very fecund currency, and there are also Euromarks and Euroyen and Eurofrancs, all looking rested and tanned and showing no desire to go home.

The problem with those Eurodollars is that they *could* come home; they did not have to stay contained in their own wonderful world. What if there were too many of them?

Adam Smith, "Paper Money", pp. 121-125